Vietnam's banking sector entered 2026 with strong growth momentum, supported by GDP growth of 7.8% in year’s first quarter (Q1), the highest first-quarter rate since 2019. The State Bank of Vietnam held its refinancing rate steady at 4.5%, maintaining the accommodative stance in place since June 2023, and set a full-year credit growth target of 15% for 2026.

The 26 Vietnamese banks reporting Q1 2026 results saw operating income rise 16% year on year, up from 6% in Q1 2025, while pre-impairment operating profit increased 19%, compared with 4% a year earlier. Pre-tax profit growth remained solid at 13%, slightly below 14% a year earlier, as provision charges rose 18% following a 4% decline in Q1 2025. A one-off gain at SeABank also influenced the overall figures, as the bank booked a profit in Q1 2025 from the sale of PTF Finance to AEON Financial Service. Of the 26 reporting banks, 19 recorded year-on-year growth in pre-tax profit, while seven reported declines.

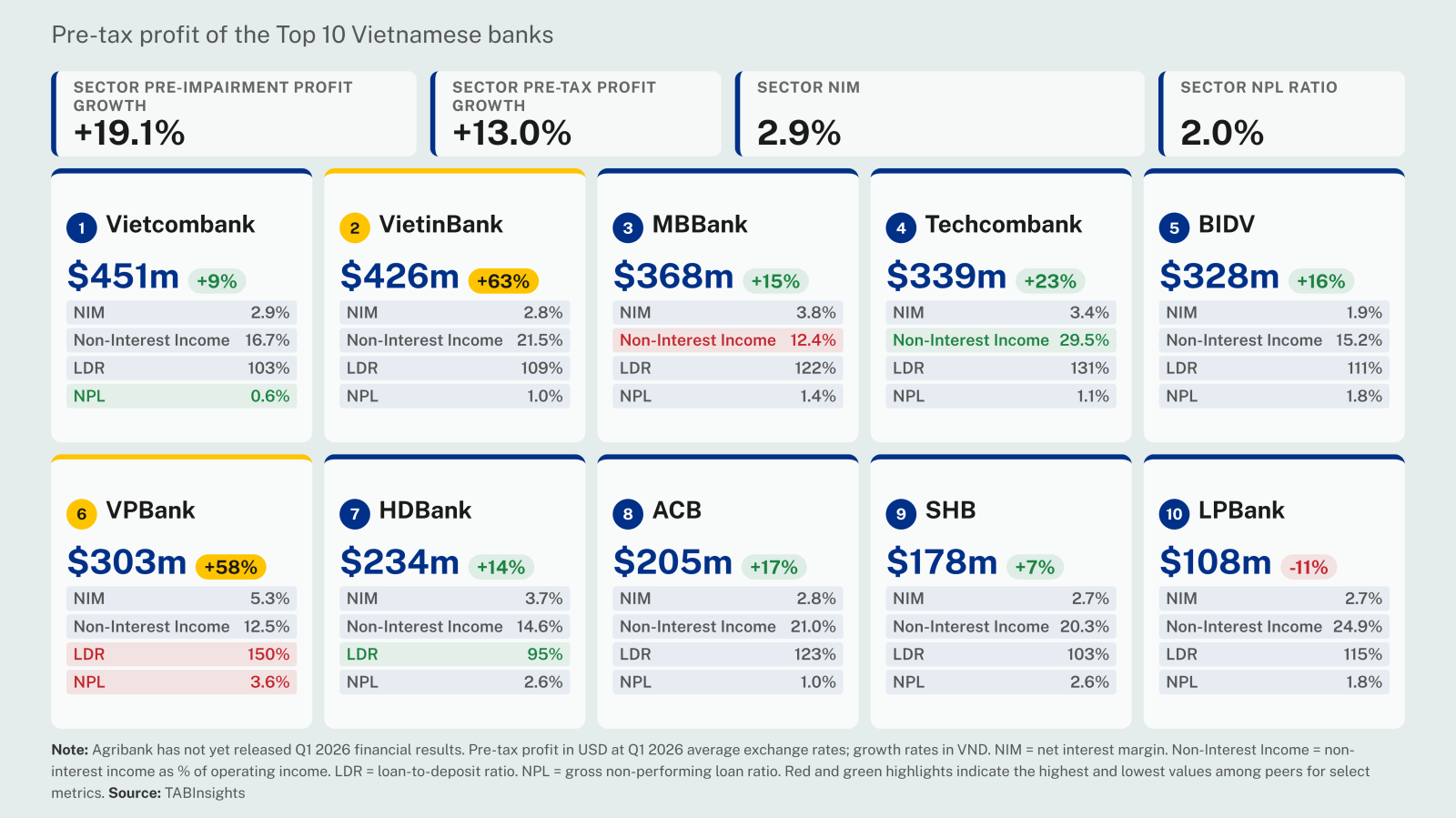

Vietcombank records the highest profit, while VietinBank and VPBank post strong growth

Vietcombank posted the highest pre-tax profit in absolute terms, reaching VND 12 trillion ($451 million) in Q1 2026. Operating income grew 23%, but pre-tax profit rose only 9% as provisions tripled to 17% of pre-impairment operating profit. The higher provisioning strengthened an already robust balance sheet, with the non-performing loan (NPL) ratio falling from 1.0% in Q1 2025 to 0.6% in Q1 2026 and the provision coverage ratio rising from 216% to 253%.

VietinBank recorded the second-highest pre-tax profit and led growth among large banks, rising 63% in Q1 2026. A 25% increase in net interest income and a 5% decline in provision charges supported performance, while provisions still accounted for 42% of pre-impairment operating profit. Its NPL ratio fell from 1.6% to 1.0%, and the provision coverage ratio rose from 137% to 167%.

MBBank and Techcombank ranked third and fourth in pre-tax profit, with growth of 15% and 23%, respectively. At MBBank, provisions increased 38%, accounting for 21% of pre-impairment operating profit, whereas Techcombank's provisions declined 9% to 8% of pre-impairment profit.

VPBank grew pre-tax profit by 58%, despite recording the sector's second-largest provision charge at VND 7 trillion ($260 million), equivalent to 45% of pre-impairment operating profit. Its net interest margin (NIM) of 5.3%, the highest among reporting banks, together with 81% growth in fee income, underpinned robust profitability.

SeABank and Eximbank recorded the largest profit declines. SeABank's pre-tax profit fell 68%, largely due to a one-off gain in Q1 2025 from the disposal of its stake in PTF Finance to AEON Financial Service. This strategic divestment supports capital restructuring and a sharper focus on core retail banking. Eximbank's pre-tax profit dropped 59%, with net interest income rising only 2% and non-interest income down 85%. Provision charges surged 800%, accounting for 40% of pre-impairment operating profit.

Asset quality remains stable, but pressures are uneven

The sector's asset quality remained broadly stable, with the average NPL ratio improving slightly to 2.0% in Q1 2026 from 2.1% in Q1 2025. Higher provisions across the sector reflected both proactive buffer-building at stronger banks and reactive adjustments at weaker institutions, directly influencing earnings.

Vietcombank, Asia Commercial Bank, VietinBank and Techcombank maintained the strongest asset quality, with NPL ratios ranging from 0.6% to 1.1% and provision coverage ratios from 114% to 253%, supported by conservative underwriting, diversified loan portfolios and higher recovery capacity. Fifteen of the 26 reporting banks recorded NPL improvement.

In contrast, NCB, SaigonBank, PGBank, BVBank and Vietbank reported NPL ratios above 3% and provision coverage ratios below 50%, highlighting continued pressure on earnings at weaker banks. NCB's NPL ratio improved to 7.2% from 14.0%, but its provision coverage ratio remained low at just 18%. Sacombank's NPL ratio deteriorated the most, rising to 6.6% from 2.5% in Q1 2025 due to legacy asset reclassification.

Funding pressures and low fee income share constrain profitability

The sector's net loan-to-deposit ratio (LDR) rose to 114.2% in Q1 2026 from 107.9%, as loan growth outpaced deposits amid strong competition for market share. Loan growth slowed to 19% in Q1 2026 from 21% in Q1 2025, while deposit growth eased to 13% from 16%. Only six of the 26 banks had LDRs below 100%, while VPBank and Techcombank reported the highest ratios at 150% and 131%, respectively. This reflects stronger competition for deposits and greater reliance on the interbank market and bond issuance. Higher funding costs compressed the sector's NIMs from 3.1% in Q1 2025 to 2.9% in Q1 2026.

Margin pressure varied across institutions. VPBank and HDBank maintained high NIMs at 5.3% and 3.7%, respectively, supported by consumer and agricultural lending, while MBBank and Techcombank recorded NIMs of 3.8% and 3.4%, benefiting from strong current account, savings account (CASA) bases. In contrast, BIDV remained constrained by policy-directed lending, with a NIM of just 1.9%.

Meanwhile, the sector's fee income share of operating income remained low. Net fee and commission income rose 38%, increasing its share of operating income from 9.4% to 11.1%, driven by bancassurance, digital banking and payments. Other non-interest income fell 14% due to weaker foreign exchange and trading activity. Techcombank generated the largest absolute fee income at VND 3.1 trillion ($120 million), followed by VPBank at VND 2.1 trillion ($79 million). VIB posted the fastest growth, with fee income surging 427% to VND 2.0 trillion ($76 million), accounting for 36% of operating income.

Profit growth expected to maintain double-digit pace despite pressures

Profitability in Vietnam's banking sector is expected to remain under pressure throughout 2026, driven by rising funding costs, tighter liquidity conditions and asset quality concerns. Sector NIM is likely to stay below 3% as faster loan growth relative to deposits keeps funding costs elevated. Asset quality pressures are expected to re-emerge as the effects of earlier aggressive write-offs and rapid credit expansion normalise. Credit growth is projected to moderate from 2025 levels amid a high credit-to-GDP ratio above 140% and regulatory tightening, including stricter lending quotas and limits on real estate exposure, while Basel III capital requirements will influence lending capacity across banks.

Large banks with stable deposit franchises, strong capital buffers and broad funding bases are better placed to sustain growth and absorb credit costs. Smaller lenders, by contrast, are likely to face continued pressure from higher funding costs, rising provisioning needs and slower loan expansion. Overall, sector profit is still expected to grow at a double-digit pace, but divergence across banks is likely to widen.

.png)

.png)

.webp)