_Webbanner.webp)

Research Notes

Jul 16

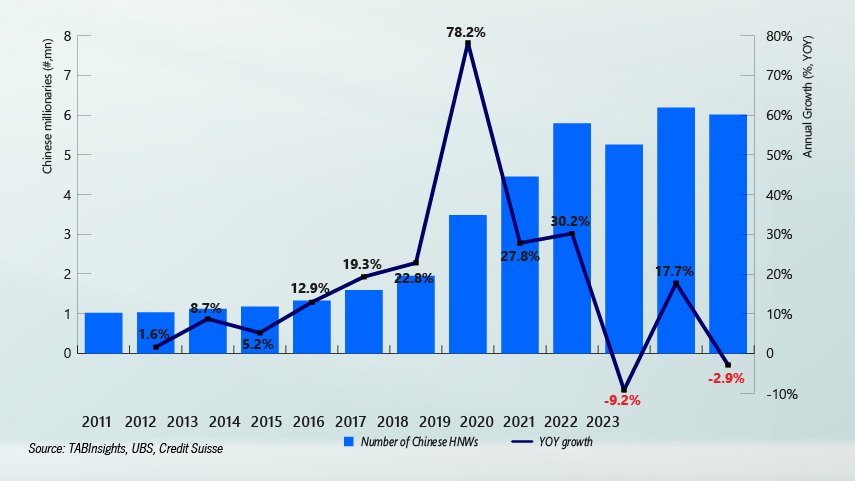

China’s retail banking sector faces regulatory and macroeconomic pressures that are lowering revenues and profits, with banks turning to AI and technology to boost growth and customer engagement