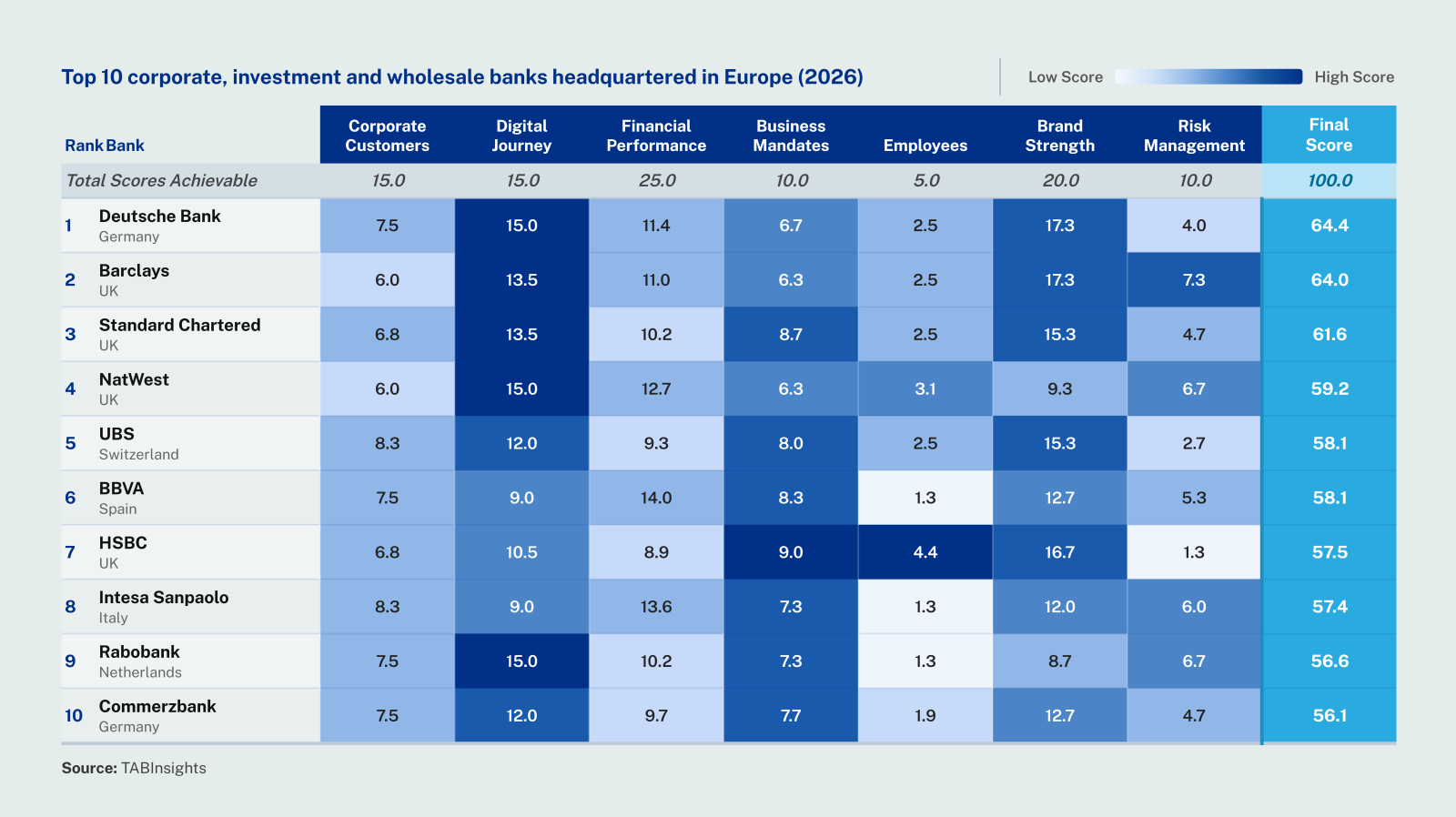

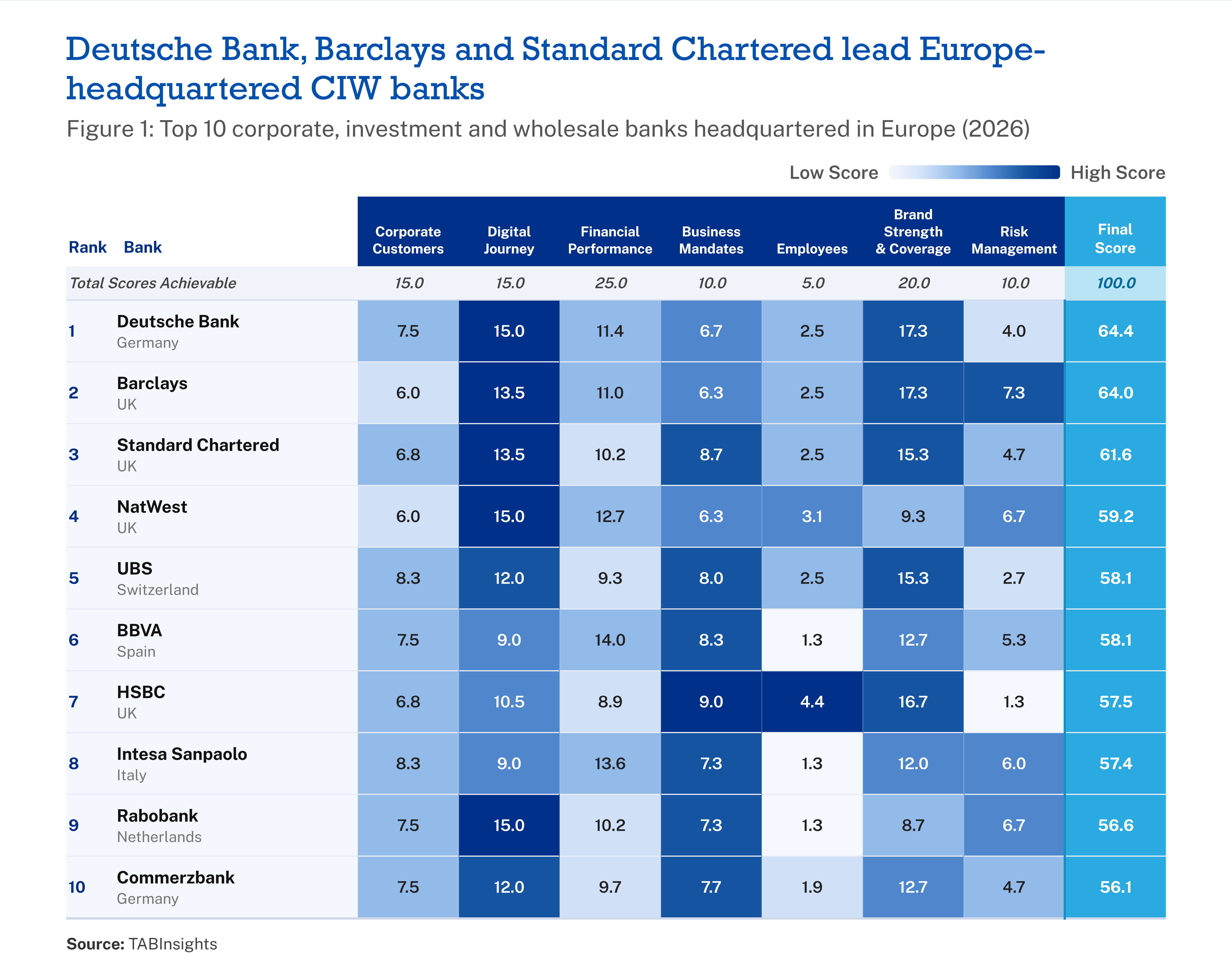

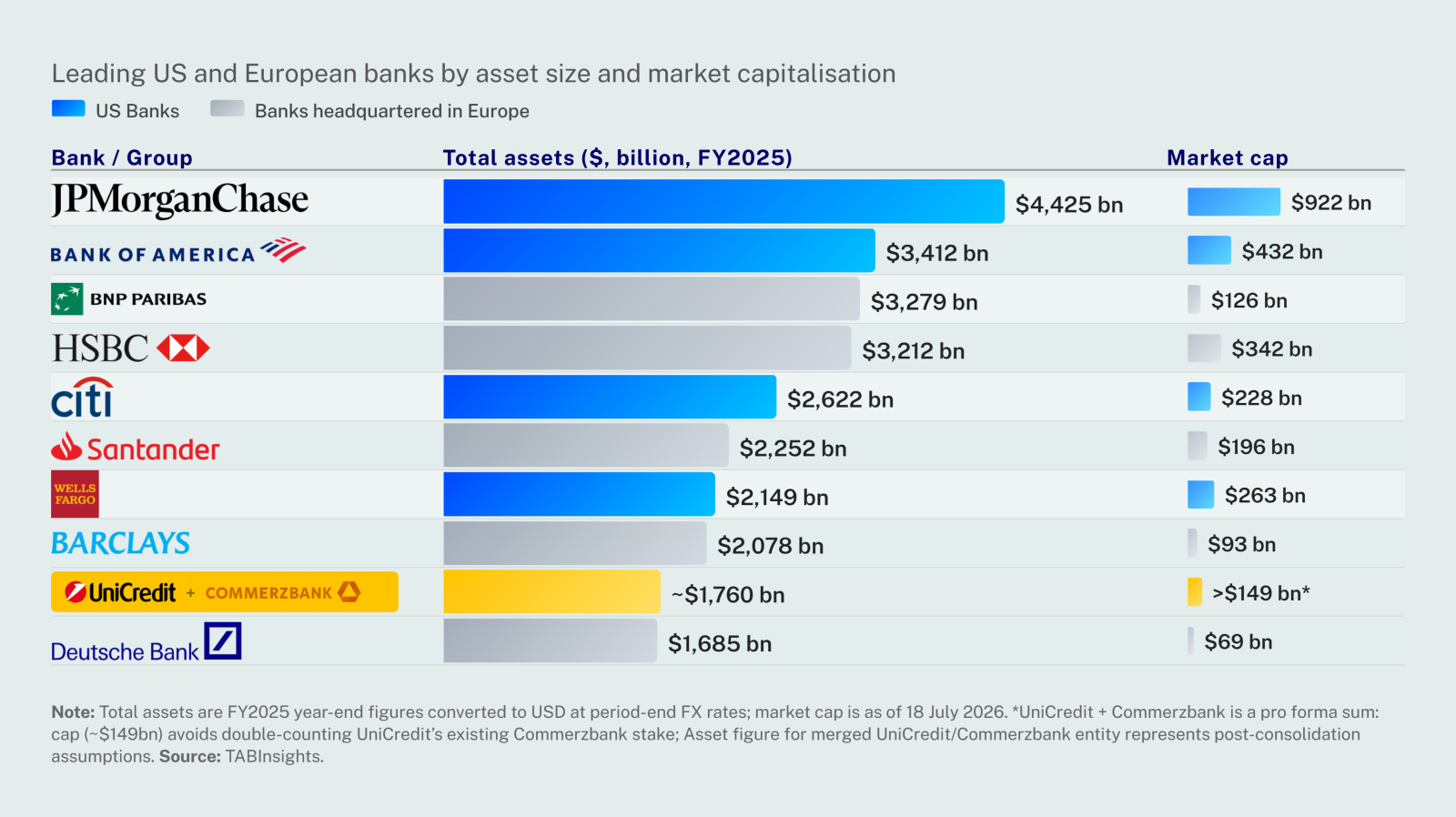

In the 2026 TABInsights World's 100 Best Corporate, Investment and Wholesale (CIW) Banks Ranking, Deutsche Bank leads among institutions headquartered in Europe, with Barclays in second place. The top 10 institutions based in Europe together generated approximately $132 billion in combined CIW revenues, equivalent to 14.5% of the $912 billion recorded across the full ranking.

Deutsche Bank claims the top position among institutions domiciled in Europe on the strength of its digital journey performance, financial results, corporate client franchise and brand coverage. The bank upgraded its digital corporate banking infrastructure in 2025, integrating liquidity, foreign exchange and payment solutions through its dbX platform and introducing a digital know your customer (KYC) portal for corporate clients. This strengthened digital engagement across its corporate client base. Revenue grew 5% to $21 billion in 2025, while its cost-to-income ratio (CIR) improved to 60% from 65% in 2024, reflecting its ongoing efficiency improvements. Pre-tax profit rose 28% to $7 billion, underscoring the strength of the franchise even as the bank continued to invest in structural improvement.

Barclays placed second, with CIW revenues accounting for 52% of total revenue, underlining the centrality of its wholesale franchise to group performance. The bank generated $20 billion in CIW revenues in 2025, up 11% year on year. Growth was driven by strong performance across its Investment Bank and expansion in its International Corporate Bank, supported by increased transaction banking and leverage finance activity. Its CIR improved to 61% in 2025 from 65% in 2024, reflecting stronger revenue growth across wholesale segments and continued cost discipline.

Standard Chartered placed third, with a broad multi-market presence and the second highest business mandates result in the group. The bank generated $12 billion in CIW revenues, up 5% year on year, and deployed SC GPT across 41 markets, empowering over 70,000 employees. Its CIR stood at 53% in 2025 from 55% in 2024, reinforcing its position as one of the more efficient wholesale banking franchises in the European cohort.

HSBC held the largest segment asset base in the European top 10 at $2 trillion. It recorded the highest business mandates result across the group, and generated $28 billion in CIW revenues in 2025. Despite leading on revenue, HSBC's overall ranking reflected a multi-dimensional scoring framework in which digital journey performance and cost efficiency weighed alongside financial scale. Its CIR rose to 56% from 55% in 2024, driven by $1 billion in restructuring costs tied to its organisational simplification programme and higher technology investment.

NatWest’s investment in digital infrastructure contributed to stronger financial performance. Revenue rose 11% to $12 billion in 2025, supported by strategic partnerships with AWS, OpenAI and Google and the establishment of an AI Research Office. Pre-tax profit rose 13% to $5 billion and its CIR improved from 54% to 51%.

UBS generated $16 billion in revenues, up 9%, as Credit Suisse integration costs continued to normalise, bringing its CIR down from 77% to 75% and improving pre-tax return on assets (ROA) from 0.5% to 0.6%. BBVA's sector-specialisation model and AI-led client advisory initiatives supported broad-based growth across its corporate and institutional franchise.

Intesa Sanpaolo's disciplined cost management, reflected in a decline in operating costs in 2025, combined with fee and commission income growth, drove a marked improvement in profitability. Rabobank's performance was supported by its digitally engaged corporate client base, lifting revenues to $5 billion while improving its CIR to 53% in 2025 from 57% in 2024.

Commerzbank was the only institution in the European top 10 to record a revenue decline in 2025. Nevertheless, it maintained its ranking through balanced performance across corporate client engagement, business mandates and brand coverage across nearly 40 markets. Its digital journey was supported by an expanding AI programme, including Agent Assist and cobaGPT, which have been deployed to more than 30,000 employees.

While these results affirm Deutsche Bank's leadership among institutions headquartered in Europe, they also sit within a broader global context. The largest banks based in the United States continue to operate at a materially different scale, even within the European market itself. JPMorgan Chase, for instance, generated $78.5 billion in CIW revenues globally in 2025 with a 3.9% global revenue market share, a reminder that the competitive landscape within Europe extends well beyond institutions based in the region.

Across the leading CIW banks domiciled in Europe, digital capability, operating efficiency and franchise depth are becoming increasingly interconnected drivers of competitive advantage. Institutions that continue to improve productivity while investing in digital transformation are best positioned to sustain ranking performance. Risk management remains the dimension with the greatest variation across the group, presenting the most significant opportunity for upward mobility.

View the World’s 100 Best Corporate, Investment and Wholesale Banks Ranking here.

Subscribe for regular insights.

.png)

.webp)