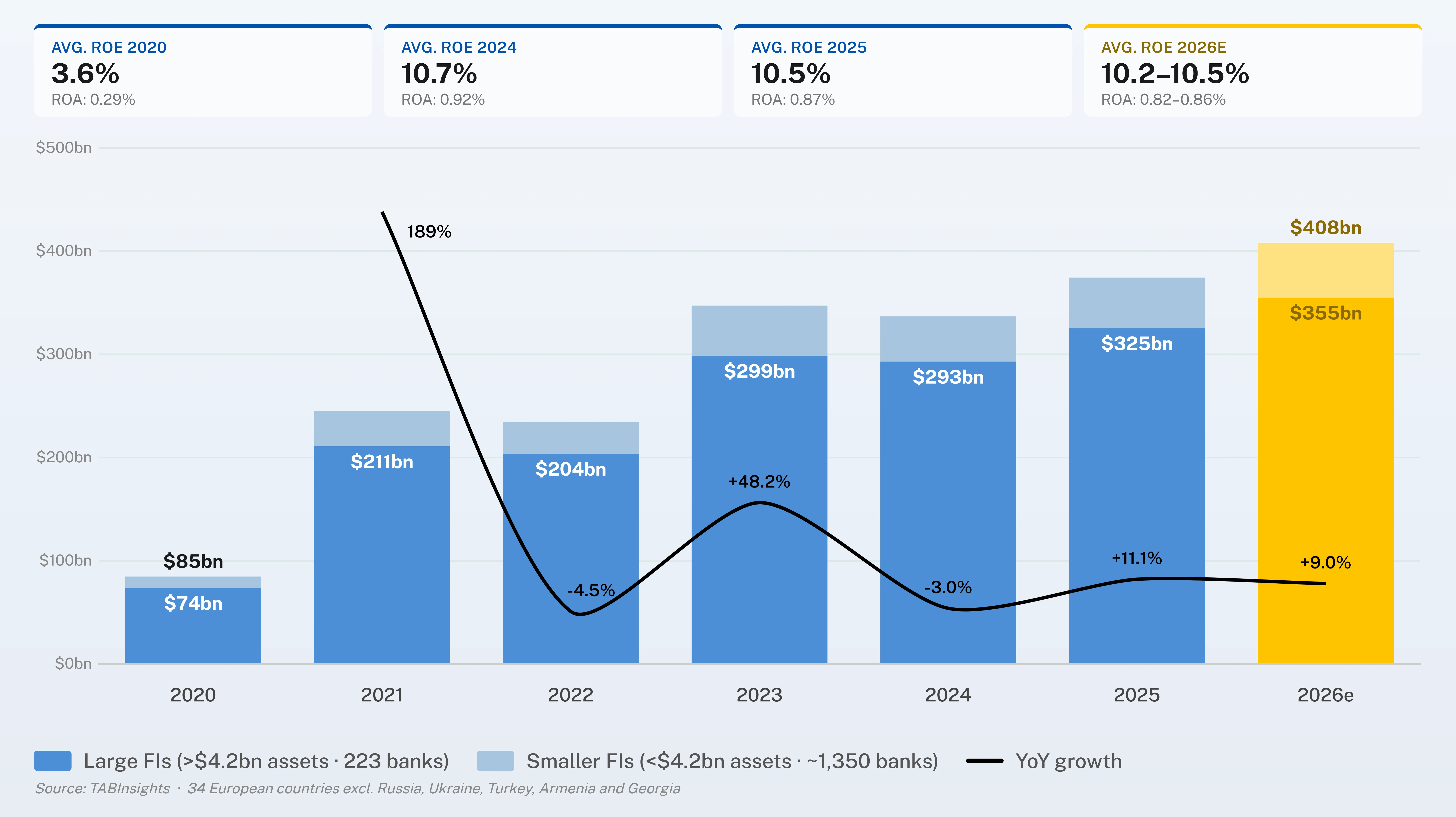

The macroeconomic outlook for 2026 remains uncertain, with both the European Central Bank (ECB) and the International Monetary Fund (IMF) revising downward their growth forecasts for the Eurozone amid rising geopolitical risks. The ECB projects baseline gross domestic product (GDP) growth of 0.9%, while the IMF has reduced its Euro area growth forecast to 1.1%, reflecting concerns over energy supply disruptions linked to the Middle East conflict and sustained pressure from higher oil and gas prices. Despite the weaker outlook, the European banking sector’s net profit is still expected to reach a record $408 billion in 2026, up 9% year on year under a mild-impact scenario.

Before the conflict, the European Banking Authority’s (EBA) December 2025 risk assessment report, covering around 160 banks, provided one of the clearest forward-looking signals for the sector: 67% of European Union (EU) banks said they do not expect further growth in return on equity (ROE) in 2026, with strategic priorities shifting towards cost control and the expansion of non-interest income.

Net profit is expected to reach $408 billion in 2026

Figure 1. Industry net profit of European banks (2020–2026e, $, billion)

Note: Europe has about 5,300 licensed deposit-taking institutions, but only 400–600 are material by assets and earnings. TABInsights tracks 223 banks across 34 countries in detail, each above roughly $4.2 billion in assets, covering about 86%–87% of system assets. Adding the next 280 banks, with assets of $1 billion to $4.2 billion, would lift profit coverage by about 8–9%. The remaining 1,000–1,400 sub-$1 billion institutions account for only 3–4% of assets, and likely less of profits because of weak scale economics. Figures are based on 34 European countries excluding Russia, Ukraine, Turkey, Armenia and Georgia.

Source: TABInsights

Against the current backdrop, the industry’s ROE for 2026 is projected to range between 10.2% and 10.5%, broadly in line with 2025 levels. Uncertainty over the duration of the crisis is expected to prompt banks to strengthen capital positions, preserve balance sheet flexibility and increase forward-looking provisions.

European banks’ direct exposure to the Middle East remains limited, with risk largely concentrated among global lenders such as HSBC and Standard Chartered, which set aside provisions of $300 million and $190 million respectively in Q1 2026 to account for geopolitical and macroeconomic uncertainty. By contrast, most European banks have negligible direct exposure to Iran and only limited direct regional risk.

The more material threat to profitability stems from indirect channels, including higher oil prices, persistent inflation, supply-chain disruptions, weaker corporate confidence, and rising credit losses and provisions. In this context, the primary residual risk for European banks in 2026 is no longer monetary policy but the credit channel. Small and medium-sized enterprises (SMEs) accounted for €32 billion ($37.7 billion) of non-performing loan (NPL) inflows in the first half of 2025 alone, the largest single contributor, concentrated in tariff-sensitive manufacturing, according to the EBA.

In 2025, European banks have outperformed expectations, defying concerns that declining interest rates would weigh on profitability. The sector recorded 11% year-on-year (YoY) growth in net profit, even as net interest margins (NIMs) compressed by 10 basis points between 2024 and 2025. Despite 200 basis points of ECB rate cuts, earnings were supported by improved cost efficiency, stable asset quality, and cost of risk remaining near historic lows.

First-quarter 2026 results for the largest European banks came in stronger than expected, with most major lenders posting solid YoY profit growth. Spain’s BBVA reported an 8% increase in net profit, while the UK’s HSBC and Barclays recorded gains of 12% and 16%, respectively. In Italy, UniCredit posted a 16% year-on-year rise, and Germany’s Commerzbank reported a 9% increase. In Belgium, KBC Group delivered net profit growth of 12.8%, underscoring broad-based earnings resilience across the region’s banking sector.

The key question is whether a prolonged conflict in the Middle East will weigh on full-year expectations. Using a mid-range sensitivity of a 4% net profit reduction for each one percentage point shortfall in GDP, and assuming 0.4% reduction in Eurozone growth in 2026 (from 1.4% to 1.0%) implies an estimated 1.6% drag on sector profits. Alongside slower loan growth, higher expected credit losses and provisions, and increased energy-related operating costs, these pressures may be partly offset by stronger fee income in wealth and asset management, trading revenues, and a potentially firmer interest rate outlook for the remainder of 2026. As a result, the European banking sector’s 2026 profit growth forecast has been revised to 9%, down from a pre-conflict estimate of 10%.

Banks with durable non-interest income show more stable earnings across the cycle

The European banking sector’s median non-interest income share across 223 banks declined from 34.3% in 2020 to 28.7% in 2024, reflecting faster growth in net interest income (NII) during the interest rate upswing. This compression is now reversing: as NIMs normalise, banks without a durable fee income engine face renewed pressure on revenue.

Analysing 223 of Europe’s largest banks between 2020 and 2024, those in the high non-interest income tertile—averaging more than 38% of operating income from non-interest sources—achieved a higher mean ROE of 8.1%, compared with 7.2% for banks with less than 27% non-interest income. While the difference is modest, a more diversified income mix helps dampen the impact of interest rate cycles on returns.

Among larger institutions, the “double winners”—banks that maintained non-interest income above 38% of operating income while keeping ROE volatility low across the 2020–2024 cycle—are concentrated in the Nordics and Belgium. In Sweden, Skandinaviska Enskilda Banken (SEB) averaged an ROE of 14.3% with low volatility, sustaining a minimum non-interest income share of 41% over the period. In Belgium, BNP Paribas Fortis, a subsidiary of BNP Paribas, increased its non-interest income share from 41% in 2020 to 56% in 2024—the largest gain among large European banks—while delivering a mean ROE of 10.2% with a standard deviation of just 1.5 percentage points, the most stable performance in the large-bank cohort.

Cost restructuring and technology investment represent a third pillar of performance and arguably the least fully priced by the market. Across the European banking sector, large-scale efficiency programmes are underway, combining branch rationalisation, back-office automation and accelerating AI adoption. Productivity gains from these initiatives are beginning to filter through into cost-to-income ratios, particularly among Nordic and Eastern European (EE) banks, which lead the sector on efficiency metrics. Nordic cost discipline predates the ECB tightening cycle and reflects years of sustained digital-first investment.

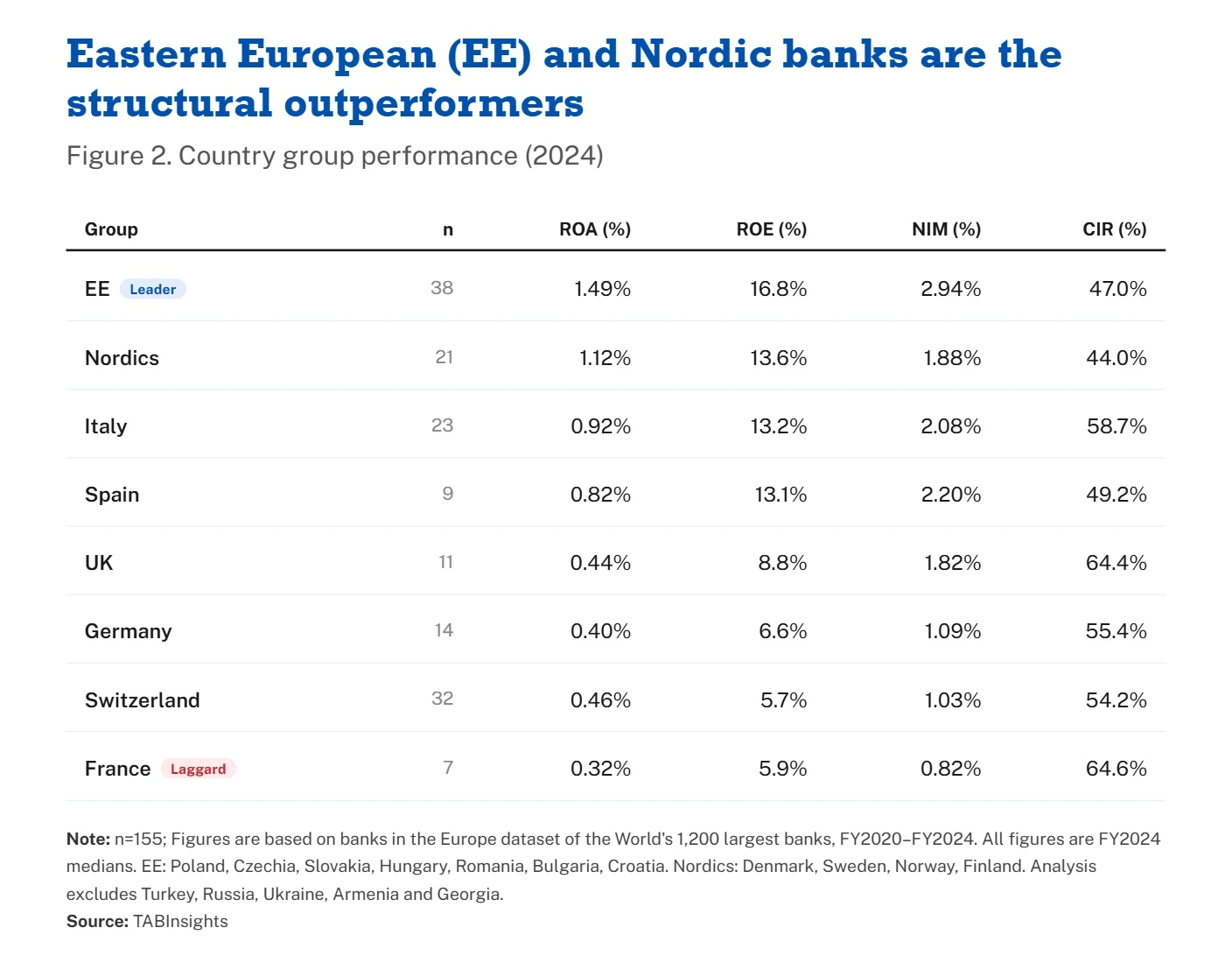

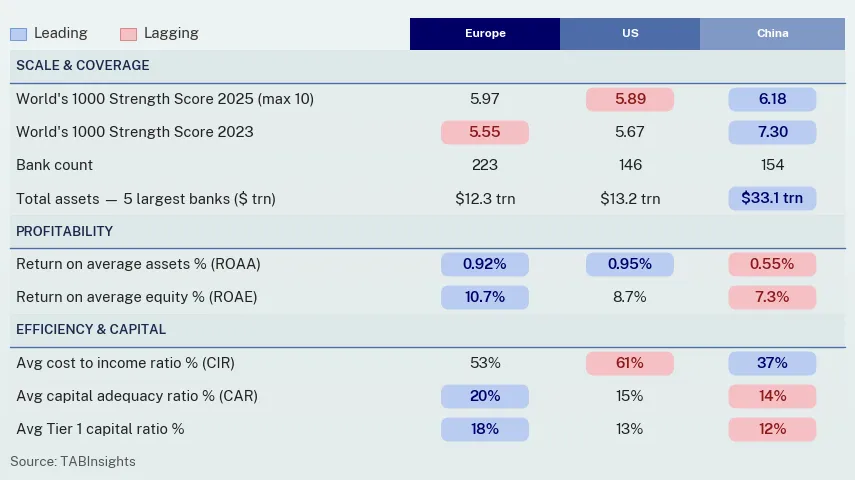

Eastern European (EE) and Nordic banks outperform European peers

Eastern European banks are the most profitable, while Nordic banks are the most operationally efficient large-market group in Europe, with a gap of more than 20 percentage points versus UK and French peers that has persisted throughout the full five-year period.

Spain and Italy, long characterised by excess capacity and legacy asset quality challenges, have materially improved their positions. Italian banks now report a median ROE of 13.2%, reflecting years of NPL clean-up, branch rationalisation and diversification of fee income. Spain records a median NIM of 2.20%, among the highest in Western Europe, supported by a retail-focused funding base that enabled a stronger pass-through of the ECB rate cycle compared with the more wholesale-funded French and German universal banks.

French banks, despite recording one of the lowest ROEs at 0.32%, paradoxically report the highest non-interest income share at 50.3%, reflecting substantial capital markets, insurance, and asset management franchises. Their challenge is not revenue diversification but cost structure, with a median cost-to-income ratio (CIR) of 64.6%, which the rate cycle has done little to improve.

Profit outlook for European banks clouded by geopolitical risk and rate normalisation

Three dynamics will determine whether the $408 billion profit projection for 2026 is achieved. First, the credit channel has emerged as the principal residual risk: SME NPL inflows recorded in the first half of 2025 are likely to accelerate in 2026, with the pace of provisioning over the remainder of the year set to be a key determinant of full-year earnings.

Second, if the Middle East conflict leads to sustained disruption in energy supply chains through mid-2026, a scenario economist Paul Krugman described in April as increasingly plausible, the implied 1.6% earnings drag embedded in current assumptions could prove understated, potentially pushing sector-wide profit growth below the revised 9% forecast range.

Third, the efficiency gap between Nordic and Eastern European banks on one side, and French and German universal banks on the other, is expected to widen further as AI-driven back-office investments begin to feed through more visibly into cost-to-income ratios by 2027.

Overall, European banks may see some near-term benefit from a potential rise in interest rates in June, although this would also increase expected credit loss assumptions. Banks with less than 30% non-interest income are particularly exposed to rate normalisation once geopolitical tensions ease. In this context, SME credit portfolios remain the most vulnerable segment, while high cost-to-income universal banks in France and Germany may need to accelerate restructuring efforts before earnings buffers narrow further.

.png)